3.5 Weeks

Average Project Timeline

Talk to an Expert

It’s no easy feat to write a business plan that meets lender and Small Business Administration standards for 7(a) or CDC/504 loan programs. Click the button below and we will email you three full example PDFs of our bank- and SBA-targeted work.

A professional business plan helps investors to understand and believe in your business. Click the button below and we will email you three full example PDFs that will demonstrate proper structure, analysis, and narrative to capture and retain investor attention.

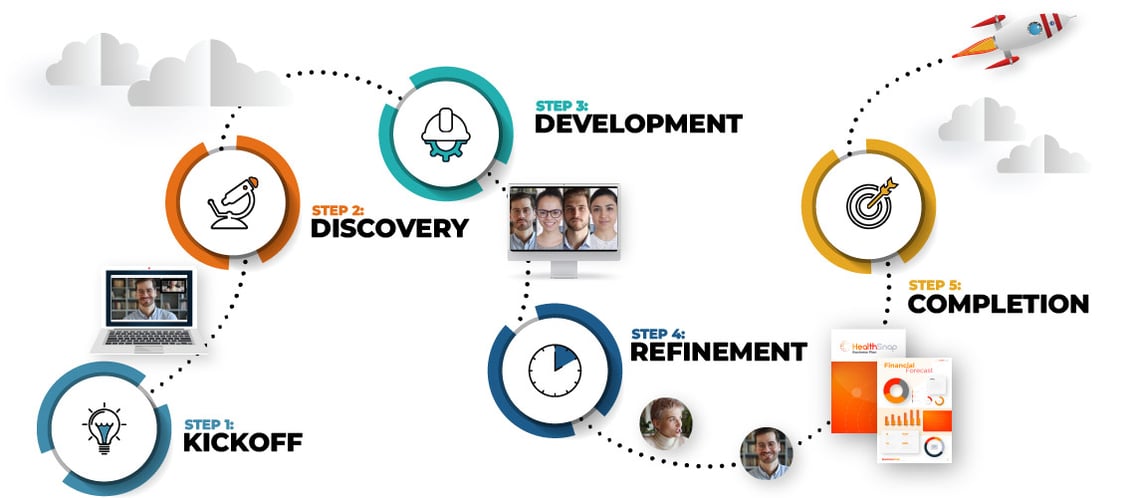

It's not easy to put together a business plan that hits all of your targets. With that in mind, our team created this comprehensive business plan Q&A to help you along the way. But if you get stuck or need help, don't be afraid to call on our experts.

Contact Us