Business Plan 101

All the answers to your questions about how to write a business plan from the professionals who write them every day

Almost everyone is familiar with the term “business plan.” However, for some reason, this crucial foundational business document is shrouded in mystery. No longer.

Below is a list of frequently asked questions from our clients, which we hope will provide insights into your business planning journey. And if we missed something, please send us an email with your business plan question and we will get back to you (and perhaps even add your question to our list).

-

How much does it cost to start a business?

The cost of launching a business varies greatly depending on the type of business, location, and a variety of other factors. Some businesses can be started with very little money, whereas others require a substantial investment. Here are the most common types of startup costs for new businesses:

- Business registration: These may include the cost of registering your business name, obtaining any required licenses and permits, and establishing any legal structures such as a corporation or LLC (see "What business structure should I use?").

- Business insurance: Business insurance safeguards your company in the event of a lawsuit or other unforeseen event. Businesses may require various types of insurance, including general liability insurance, errors and omissions insurance, property insurance, and vehicle insurance.

- Physical space: If you intend to open a physical location for your company, you will have to pay for rent, utilities, and any necessary renovations or remodeling (usually referred to as "buildout"). Even if you do not require a separate location for your business, any changes you make to your home are covered here.

- Equipment: Depending on the type of business you plan to launch, it may be necessary to purchase equipment. Equipment includes computers and all other fixed assets, such as machinery and vehicles.

- Fixtures & Furniture: In addition to equipment, fixtures and furniture are often required as additional fixed assets (these three items are frequently grouped together as "FF&E"). In most cases, a fixture is something that is permanently attached to the space, whereas furniture can be easily moved. A built-in shelving unit, for example, is a fixture, whereas a free-standing desk is furniture.

- Inventory: If you sell any type of product, you will need to purchase (and maintain) inventory, which includes finished goods that you buy at wholesale prices as well as raw materials that you use to make finished goods. The amount of inventory you require will depend on the type of business you have and is considered a current asset.

- Marketing and advertising: Most businesses need some sort of online presence, most often in the form of a website. Additionally, the majority of businesses will create a formal brand that represents their values or products. The costs of marketing and advertising can vary greatly. Some businesses sell their products on well-known platforms such as Etsy, which requires little to no upfront payment, whereas others may require a full-fledged ecommerce website, which can cost thousands of dollars. Other industries may require extensive television advertising campaigns.

- Professional fees: These include any legal, accounting, or consulting you need to launch your business.

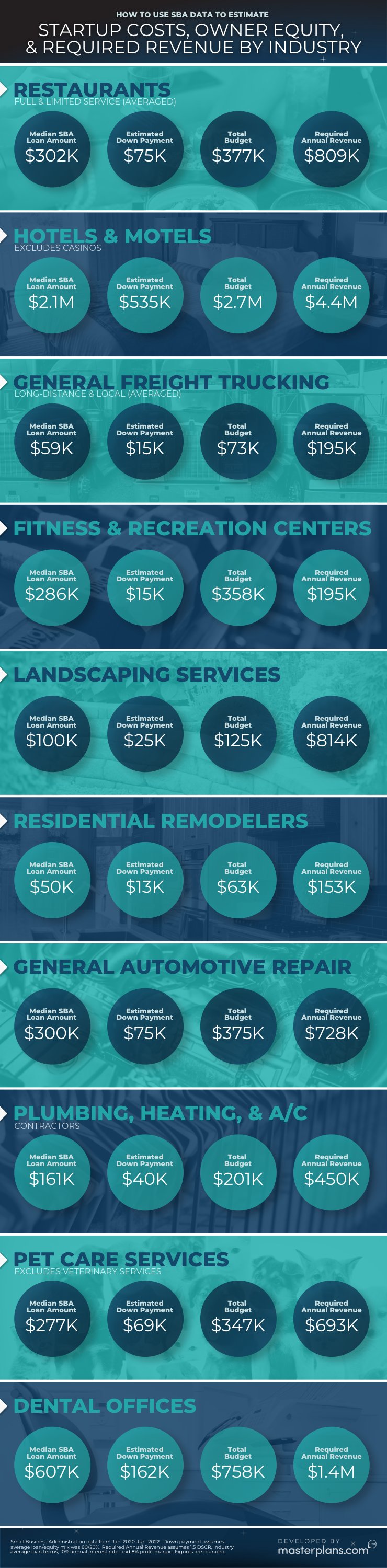

Curious about what it typically costs to start different kinds of companies? Masterplans analyzed SBA data to figure out the average startup cost of the top 10 most common new businesses (you can also download our startup costs infographic). -

Is a business plan necessary to get funding?

We’ve all heard apocryphal stories about Amazon getting funded based on a diagram scribbled on the back of a napkin over lunch with a potential investor. And the term “elevator pitch” implies that you can just pitch an idea to an investor in an elevator and get money on the spot. But the chances of this happening are so slim as to be laughable, and you certainly wouldn’t want to stake your business’ potential success on a napkin diagram. If you’re serious about your idea, you need to treat it seriously, and that means taking the requisite steps to show that you’re worthy of investment.

-

What are the different ways to fund a business?

While there are numerous ways for an entrepreneur to fund a business, the following is a summary of the most common methods. Remember that your company does not have to choose just one method; many of the most successful startups combine multiple funding types depending on the amount, timing, and initiative, and so on.

Bootstrapping

Many entrepreneurs start and grow their businesses with their own savings and investments. Self-funded businesses frequently rely on credit cards and small loans from family and friends to supplement their own funds. Bootstrapping allows entrepreneurs to grow their businesses organically, but it can be difficult due to a lack of cash flow.

Pros of bootstrapping:

- Full control

- Less risk

- Flexibility

- Lower cost

- Faster startup

Cons of bootstrapping:- Limited funding

- Slower growth (due to lower capititalization)

- Personal risk

- No access to mentorship and advice

Business loansBanks, credit unions, and other financial institutions provide a range of business loans, including term loans, lines of credit, and SBA loans. The most common loan type is a term loan, in which a business receives a lump sum of money and repays it with interest and principal payments over a set period of time. SBA loans are a specific type of term loan designed to provide small businesses with greater access to capital. SBA loans are partially guaranteed by the government, making them ideal for entrepreneurs who may be unable to obtain a conventional term loan. A second type of loan is a line of credit (LOC), which functions similarly to a credit card. The company is given a credit limit that it can use as needed while only paying interest on the amount borrowed. The final type of loan, known as invoice financing or merchant advance loans, is a hard money loan that provides cash up front against unpaid business. The interest rates on these loans are extremely high.

Pros of bank loans:

- Maintain ownership

- Provide capital to start or expand

- Consistent repayment schedule

- Establishes credit history

Cons of bank loans:- Strict qualifications (credit score, etc.)

- High interest (especially on hard money loans)

- Long-term commitment

- Requires down payment

CrowdfundingThe introduction of platforms such as Kickstarter and Indiegogo has increased the popularity of crowdfunding, especially for consumer goods. Typically, the entrepreneur establishes a campaign goal and offers incentives in exchange for contributions, which are frequently in the form of early access to or perks for the company's product. Equity crowdfunding is less common, in which individual investors contribute to the business in the form of equity and eventually receive dividends from the company's profits.

Pros of crowdfunding:

- No equity dilution

- Validates products or service

- Connect with potential customers

Cons of crowdfunding:- No funding guarantee

- Platform fees

- Expensive rewards

- Legal and regulation requirements

Angel InvestorsAn angel investor is a high-net-worth individual (HNWI) who provides capital to early-stage or startup companies in exchange for ownership equity or convertible debt. Individual angel investors, as opposed to institutional investors, typically invest their own money. Angel investors typically provide seed capital to entrepreneurs and startups at an early stage when traditional lending sources are unavailable. Angel investors seek high returns on their investment (i.e., outperforming the stock market), and therefore are willing to take on more risk than, say, a bank would. Angels can also offer mentoring, expertise, and access to professional networks to assist entrepreneurs in growing their startups.

Pros of angel investors:

- Typically passive investors

- Less focused on exit

- Mentorship and networking

Cons of angel investors:

- Seek high returns

- Can be difficult to find

- Dilutes ownership equity

- Legal requirements

Venture CapitalVenture capital firms (VCs), like angel investors, invest money in exchange for equity in the company. However, venture capitalists are typically institutional investors who pool funds from pension funds, endowments, and other business groups. VCs are looking for startups and early-stage businesses with high growth potential, and usually prefer companies that have already established themselves and are ready to scale. Because VC firms are compensated based on the success of their investments, they play an active role in the strategic direction of the companies in which they invest.

Pros of venture capital:

- Large investments (typically in the millions)

- Mentorship & expertise

- Typical path for companies that eventually go public

Cons of venture capital:- High expectations

- Loss of control

- Strict milestones and performance targets

- Legal requirements

Incubators and acceleratorsAn incubator is a program that helps startups and early-stage companies grow and develop by giving them resources like office space, mentorship, and access to a network of people in the industry. They usually focus on a specific industry or type of business, such as technology or biotechnology. Similarly, an accelerator is a program that provides mentorship, usually over a specific amount of time, usually culminating in a demo day where the different members of the cohort present their companies to potential investors. Like incubators, accelerators can be focused on a specific industry, or they can be more generalized.

Pros of incubators and accelerators:

- Mentorship

- Product validation and refinement

- Networking

Cons of incubators and accelerators:- Competitive application process

- Loss of control

- High expectations

- Can require fees in the form of equity, services, and memberships

GrantsGrants are a type of funding provided by government agencies, non-profit organizations, private foundations, and industry-specific groups that allow businesses to start or expand operations without incurring debt. They are most often awarded to established companies (as in, not startups) that meet certain eligibility criteria, such as being minority- or veteran-owned businesses. As a result, grants are frequently tied to a specific purpose, such as research and development, hiring and training employees, expanding into new markets, and environmental sustainability initiatives. Working with a professional grant writer is a good way to improve your chances of success.

Pros of grant funding:- No repayment (free money!)

- Targeted funding

- Validation of business

Cons of grant funding:- Competitive

- Strict eligibility requirements

- Complex applications

- Limited use of funding

- Usually not for startups

-

What other purposes can a business plan serve aside from funding?

Most professional business plans are written with the goal of obtaining funding, typically from lenders or investors (see “What are the different ways to fund a business?”). However, there are several cases in which an entrepreneur might need a business plan.

Strategic Vision: A strategic business plan isn't all that different from a funding business plan. It should still contain nearly all of the same sections, with the exception of the request for and use of funds. It should be noted, though, that many strategic business plans are for expanding an existing business with a new initiative or department. If internal funding is required, it would make sense to have a detailed list of sources and uses of funding. Typically, company leaders and stakeholders use a strategic business plan to align their visions, inform decision-making, and track the company's progress toward meeting the objectives.

Immigration: There are a number of ways for prospective immigrants to the United States to obtain work visas and even permanent residency through starting their own businesses. These "investor visas" include the E-2, L1-A, EB-5, and EB-2, to name a few. For these immigration cases, the United States Citizenship and Immigration Services (USCIS) requires (or strongly recommends) a business plan. Each visa type has different requirements, but in general, an immigration business plan should make a clear and compelling case to immigration authorities that the business venture will provide economic benefit to the United States, such as by creating job opportunities.

Licencing: Some industries require a business plan as part of the licensing or permit application process. The cannabis industry is a well-known example: almost every state that has legalized adult-use or medical marijuana has a limited number of licenses available that require a business plan as part of the (ultra) competitive application process. Similar requirements may apply to beer and liquor stores, pharmacies, group homes, and other types of residential facilities. Check with your state and municipality to determine what specific regulations and laws govern licensing to operate for any business that you believe may be regulated, and make sure to address those in the business plan.

Recruiting: A well-thought-out business plan makes it much easier to attract business partners and top talent. If you have a great idea for a SaaS application and have industry knowledge, you might need to hire a CTO who has previously worked in a software development role to supplement your skillset. A detailed explanation of the opportunity in a business plan is an excellent way to reach out to these potential stakeholders and get them excited about the company's potential.

Communication: There are several specific situations in which a company may need to communicate its vision and strategy to outside stakeholders. Commercial landlords are increasingly requiring tenants to provide a business plan as part of the leasing process. Property owners have a vested interest in the success of their tenants. Obviously, a tenant going out of business would result in lost rent and the need to find a new tenant. However, reputation is far more significant. If a tenant goes out of business, it may indicate to future tenants that there is a problem with the location.

-

How long should a business plan be?

It should be as long as it needs to be and as short as possible. Your business plan should cover all relevant details about your business that anyone outside the company would want to know before giving you money or letting you use their physical space. But keep your reader in mind and ask yourself: when was the last time I enjoyed reading an encyclopedia? We strive to make our plans vastly more interesting than an encyclopedia, but part of that is making sure that they’re a heck of a lot shorter. Let’s face it, people have a limited attention span, which seems to be exacerbated when reading non-fiction. So the best thing you can do is keep your business plan short while covering all of the main topics in detail. There is no maximum or minimum page count, owing to the fact that there is a wide gulf between the information needed for a used book store versus a major multinational chemical manufacturing company with multiple divisions. As a very basic guideline, most traditional business plans are between 25-50 pages long. We have compiled a collection of example business plans that you can access and use as a reference for the format and length

-

How do I structure a business plan?

If you’re going to DIY this project, we recommend starting out by making an outline that includes the following sections:

Executive Summary

- Company Ownership

- Company Location

- Use of Funds

Market Analysis

Company Overview

- Market Segmentation

- Industry Analysis

- Market Need

- Competitors

- Competitive Edge

Strategy & Implementation Summary- Objectives

- Marketing Strategy

Management Summary- Biographies of key personnel

Financial Projections- Financial Assumptions

Appendix: First Year Financials

It’s a lot to cover, but don’t get discouraged! You can do this. At Masterplans we like to use Bishop Desmond Tutu’s quote about how to eat an elephant: one bite at a time! So don’t get too discouraged by that daunting list.The next thing you’re going to do is start gathering information and just put it down on paper as each piece falls into place.

Now it’s time to begin drafting. The first thing you need to know is that the Executive Summary comes last, so don’t even worry about it right now! See, things are moving along faster than you expected already.

You can focus on whichever section you feel most interested in. If the market conditions are what’s inspiring you, start there. Just research it and write about it. Make sure to use footnotes for each hard fact that you cite, and remember that there needs to be hard facts in this section! And don’t forget to use reputable sources.

Work on each section one-by one until you’re done. A business plan won’t get done in a day if you’re a novice, so be gracious to yourself. We know this is a lot of work – we do this all day long. So if you hit a wall and realize you need help, give us a call. But know that you can do this with enough time and effort. It doesn’t take a genius; it takes someone passionate and dedicated. Luckily, that’s you.

-

How do I write a business plan for an existing business?

It’s essentially the same steps as writing a business plan for a start-up, only you probably need to spend less time on steps like deciding what your business structure should be. You still need to gather information from the various places that it’s kept. For example, if you’ve outsourced bookkeeping, you’ll need to reach out to your bookkeeper for the numbers you’ll need to run your financial model. The steps are the same; all that is really different is that you have past performance that needs to be included in your plan. The primary difference between a business plan for an existing business is that it contains charts to show past performance, which a start-up obviously doesn’t have.

-

How do I write a business plan for a small business?

When you’re starting a very small business, such as a side-hustle, it can be very tempting to ask yourself “do I really need a business plan?” You might end up just skipping this step. We strongly caution against that. Every business needs a business plan, no matter how small. Use the steps outlined above under the FAQ “How do I write a business plan for a startup?”

-

How do I write a business plan for a non-profit organization?

Non-profit organizations are still businesses, even though their funding typically comes from different sources. You still need a business plan, and it should still follow the same steps outlined in “How do I write a business plan for a startup?” What’s different here is that your business will be registered as a 501(c)3 corporation, and instead of owners, you’ll have a board of directors. Additionally, though you can use your business plan for funding, you will likely be applying for grants as well, and they tend to have their own detailed requirements for what needs to be included, that vary based on the organization giving the grants. Having your business plan already written can help when it comes to applying for those grants. You can simply copy and paste the sections that apply to the grant submission requirements, saving yourself time over the long term.

When working on your organization’s financials, it’s important to note a terminology change from for-profit businesses. Instead of “profit,” you will have “surplus” and your “revenue” is called “funding.” Thus, instead of a “Profit & Loss” statement, a non-profit will have a “Surplus & Deficit” statement.

-

How do I write a business plan for a franchise?

Franchises often claim to provide you with your own business plan, but what they really provide is a document called an FDD (Franchise Disclosure Document). You will still need to follow all the steps outlined above under the FAQ “How do I write a business plan for a startup?” What’s different for you is that you will benefit from a range of support services, like location selection, marketing support, and maybe even market analysis help, depending on the franchise in question. In the end, a franchise is just like any other type of business, and you need to be able to speak in-depth about each of the core topics of a business plan.

-

How long does the SBA loan process take?

If you’re applying for an SBA-backed loan, don’t expect to get your money tomorrow. You have to go through a process that includes the application review, underwriting, loan agreement, and closing. It should take a minimum of 30 days, but it can take as long as 90 days and even longer, provided you have found a lender who wants to fund your business plan.

-

Where do business plan financials come from?

A business plan has extensive financial charts and tables to help your lender or investor understand your business model. The numbers you use when calculating your profit and loss statement and balance sheet should be real-world numbers based on research that you’ve done. The financials include start-up costs, cash flow statement, balance sheet, profit and loss, personnel costs, and a month-by-month forecast for your first year of operations.

For example, don’t just guess what your lease will be! Look at a website like Loopnet to see what properties are currently available in your desired neighborhood by size and property type. You don’t have to lease a space to write a business plan (you often need a business plan to lease a space!), but it can be a good plan to average the rent cost from the three places you like best.

For personnel costs, look at salary.com in your area to see what the average hourly rate is for the positions you need to hire. Don’t set your prices out of thin air either. Research your closest competitors and find out what they charge for similar products and services. It’s up to you to decide where you want to sit in terms of pricing; whether you’re offering an economy option or premium pricing, but knowing what your competitors charge can help you decide what’s a fair price for what you offer.

There are two primary methods for creating a revenue forecast: top-down and bottom-up. A top-down revenue projection model begins with the market and works its way down, whereas a bottom-up model begins with the business and works its way up. Choosing which method to use varies by industry, but Masterplans' financial modelers usually find a way to incorporate both techniques.

There will be times when you just don’t know a number that is needed to create your financials. It’s ok (and even can be ideal) to use industry standard data. Here at Masterplans, we have access to market research tools with detailed financial benchmarks for a broad range of industries, which helps us find good data when our clients just don’t know the answer. Whenever we get the question, “where did these numbers come from?,” the answer is usually IBISWorld, which we highly recommend. You can buy individual industry reports and look at the Key Statistics to find out about things like profit margins, financial ratios, wages, and revenue per employee.

-

What business structure should I use? ?

This is a great question for an accountant and/or lawyer, and you should definitely consult with one before making this decision. Your options are sole proprietorship, partnership, Limited Liability Company, S-Corporation, and C-Corporation.

- Sole proprietorship: We generally discourage use of the sole proprietorship for our customers, because the taxation is the same as your personal taxes, offering your business no benefits, and because this structure maximizes your liability if anything goes wrong.

- Partnerships: There are several different types of partnership that you can choose, but we rarely see these come across our desks, because they do not offer the same tax benefits as an LLC.

- Limited Liability Corporation (LLC): LLC is the king of business structures for a start-up, because it is superbly flexible, offers tax benefits, and has liability protection. You can even start an LLC as the sole owner and employee of your company!

- Corporation: Sometimes when we ask clients what their company structure is, they just say it’s a corporation without specifying what type. But there are two types, and which one you have matters. While both types allow you to issue shares, one of the primary differences is that with S-corps, you are limited to 100 shareholders and with C-corps, you aren’t limited in that way. How does this matter? Well, if you eventually decide to go public, you probably want more than 100 shareholders!

If you want to learn more about the different types of business structures, talk to a professional and read what the SBA has to say about it.

{kind=link}

Deliver your best with Masterplans.com

Free 30-Minute Consultation

Schedule a 30-minute meeting with one of our business planning experts so that we can better understand your objectives, advise you on appropriate steps or provide a business plan development proposal.